The COVID-19 vaccine is in fact an experimental medical procedure and because of this insurance companies have made void any claims relating to this “vaccine”.

The experimental trial in Australia runs until 2023 and thus it is only available due to an emergency use clause. Insurance companies are linking adverse reactions and deaths to this trial. As companies won’t pay out for injury and death due to experimental treatment it follows that such events following COVID-19 vaccination are not covered by hospital or life insurance.

Not a word of the above is true. Yet this notion is circulating on social media in the usual and predictable places. Despite it being demonstrably false and something one can refute for themselves in a few minutes, it is a notion with active supporters. Many others go further and contend that consent has not been given to be part of this experiment. Thus a breach of the Nuremberg Code is happening right before us.

Ethically relevant but not legally enforceable the Nuremberg Code remains semantically powerful. As such it is regrettably abused by anti-vaccine activists who have for years peddled the false claim that vaccines are not tested for safety and efficacy. It just so happens that global scrutiny of the development of COVID-19 vaccines also provided firm evidence of Phase III trials. This again refutes the anti-vaccine position and I touched on this last September. Yet as antivaccinationists are apt to do the facts have been twisted into falsehoods to support ongoing attacks on the COVID-19 vaccine rollout and to boost claims of further breaches of the Nuremberg Code.

Now, whilst this post isn’t focusing on Meryl Dorey and the Australian Vaccination-risks Network, it just so happens that she can assist us. On March 13th during an error-packed Under The Wire, Dorey presented a detailed performance outlining the absurdities that constitute the Nuremberg Code fallacy specific to COVID-19 immunisation. You may download the MP3 here, or listen below.

All of the points above popped up today in a thread on a COVID freedom fighter’s Facebook page. Elle Salzone is a feverishly active defender of anti-science beliefs. Elle moves from business to business, scheme to scheme and presently pushes ClearPHONE. Salzone and buddies sell the phone, claiming it provides the privacy necessary for today’s freedom fighters. How reliable a service it provides is uncertain. Elle fights with and also films police over her refusal to wear masks or remain in quarantine when necessary. But that’s okay if you decide to be a Sovereign Citizen. Elle is anti-COVID related responsibility. You can peruse her page for details on these pursuits.

Today one of her posts [Update: quietly deleted on 8 April] was screenshot by a tireless defender of reason, and thus came to my attention. It turned out to be an obvious forgery from this Allianz Product Disclosure Statement (PDS) and could be promptly demonstrated as such. The slideshow below is of the Allianz forgery and the two original parts of the document that were used in making it.

Salzone posts the forgery and states;

THIS IS EXTREMELY CONCERNING!!!!

Imagine getting the experimental shot thinking you’re protecting your health, then getting seriously injured and having no private health cover to help you and not being to sue because all vaccine manufacturers have been indemnified…

All to maybe protect you for a virus with a 99% Survival rate..

You literally can’t make this shit up..

“You literally can’t make this shit up”. In fact you can and in this case someone literally did. A quick search yielded the document in question. Even before presenting the original, un-cropped and pre-defaced, pages the text itself was screaming forgery. Insurance companies do not tend to torment font in that fashion. Apart from the caps lock, no policy section is referenced. Then there is the sneer at “vaccine” and the impossible consent self-infliction. Ouch! Finally at risk of boring you there’s that nagging bit about posting this most important development in the glossary.

Suffice it to say the above points were mentioned and a discussion took place.

Verified by multiple sources eh? The original source was “easily found” (comment now deleted) but Elle couldn’t find it. So screenshots of the original source were provided along with a link.

This resulted in an admission that it was posted in the knowledge it was a fake. Apparently however the information it conveyed is not only true but would be confirmed by Allianz if I checked;

For the record this forgery consists of four different screenshots from the original document pasted in a sequence that creates a misleading ‘preamble’ aiming to justify the bogus claims made beneath in added red font. The added text further presents existing terms from the Allianz PDS to construct a fraudulent disclosure statement. A significant amount of time and forethought has gone into this. It is a calculated work of disinformation that has succeeded in misleading vulnerable recipients of its message. The preparation date of the current Allianz Life Plan PDS is 5 march 2021. The date in the forgery is 31 July 2020, suggesting it could have been in circulation for some time.

Perhaps the most important aspect to look at is the claim that COVID-19 vaccines are part of an experimental “medical procedure”. This is frequently peddled by anti-vaccine activists and was also pushed by Meryl Dorey in the audio above. It is linked to other claims that the vaccine is not actually a vaccine. One contention is that mRNA vaccines are DNA modifying agents. Another is that viral vector vaccines [CDC] are completely experimental and also alter DNA. Despite available data on the molecular action, development, safety and efficacy of Pfizer, Moderna and AstraZeneca vaccines, antivaccinationists ignore this in favour of a conspiracy theory.

Viral vector vaccines are well understood due to decades of research and do not alter DNA. mRNA vaccines are also well understood and are incapable of altering DNA. The claim that COVID-19 vaccination is an experiment is often presented with the contention that the experiment will go on until 2023. Like all persistent falsehoods this has an element of fact to it. The reality is that in Australia both Pfizer and AstraZeneca vaccines have provisional approval from the TGA. The approval is valid for two years and the AstraZeneca vaccine will require review in February 2023. On 16 February 2021 the TGA stated;

The Therapeutic Goods Administration (TGA) has granted provisional approval to AstraZeneca Pty Ltd for its COVID-19 vaccine, making it the second COVID-19 vaccine to receive regulatory approval in Australia.

COVID-19 Vaccine AstraZeneca is provisionally approved and included in the Australian Register of Therapeutic Goods (ARTG) for the active immunisation of individuals 18 years and older for the prevention of coronavirus disease 2019 (COVID-19) caused by SARS-CoV-2. […]

Provisional approval of this vaccine is valid for two years and means it can now be legally supplied in Australia. The approval is subject to certain strict conditions, such as the requirement for AstraZeneca to continue providing information to the TGA on longer term efficacy and safety from ongoing clinical trials and post-market assessment.

Reading the final paragraph above we can see also how the claim that data is still being collected for the experimental trial is peddled around with such confidence. Yet post-market assessment is a vital part to better understand all drugs and vaccines. There’s no trial, no experiment. It’s worth noting this fallacy is at times linked to another false claim. That of emergency use provision for the vaccine. This was a contention made by one Clive Palmer, deconstructed handsomely here by ABC corona check. Palmer has not alleged the COVID-19 vaccine rollout is an experimental medical procedure. Although he has pushed fear over the absence of one, three and five year safety data.

When it comes to hospital cover, insurance companies will not cover treatments for which no Medicare Benefits are payable. This includes cosmetic surgery, experimental treatments or experimental pharmaceuticals. Medicare will cover certain clinical research studies. For insurers if the device, trial or treatment is not recognised by Medicare or the Medical Services Advisory Committee it will be excluded from standard hospital cover. Still, there is insurance and indemnity available for clinical trials. This helps us understand why the term being used to misrepresent the COVID-19 vaccine is “experimental”.

Allianz also have a strong supportive position on the COVID-19 vaccine and like Bupa offer a comprehensive series of answers to possible questions. In a May 2020 article Allianz cover in depth the importance of research in developing a COVID-19 vaccine and the role of insurance for subjects in clinical trials. This is not what we would expect from a company that would deny insurance cover for adverse reactions post COVID-19 vaccine. Thus the claim by Salzone that refusal to cover is “verified by multiple sources”, in conjunction with the initial and consequent screenshot, appears to be disinformation. Insurance companies across Australia cover illnesses requiring hospitalisation following vaccination.

This leaves the obsession with claiming a 99% recovery rate as some type of stamp of insignificance. It is a rather tired trope having emerged about a year ago. This may also be linked to the frankly appalling claim that people die “with COVID, not of COVID”. Thus fatalities are incorrectly labelled an overestimation. Given this is pushed often by those who falsely insist vaccines kill and injure on a large scale it reflects a rather bizarre lack of compassion. As pointed out by USA Today the COVID-19 fatality rate is ten times that of influenza. More so it may be a serious diagnosis depending on age and health. To this we must add the emerging problems of ‘long haul’ symptoms perhaps in as many as 32% of those who have recovered from COVID-19.

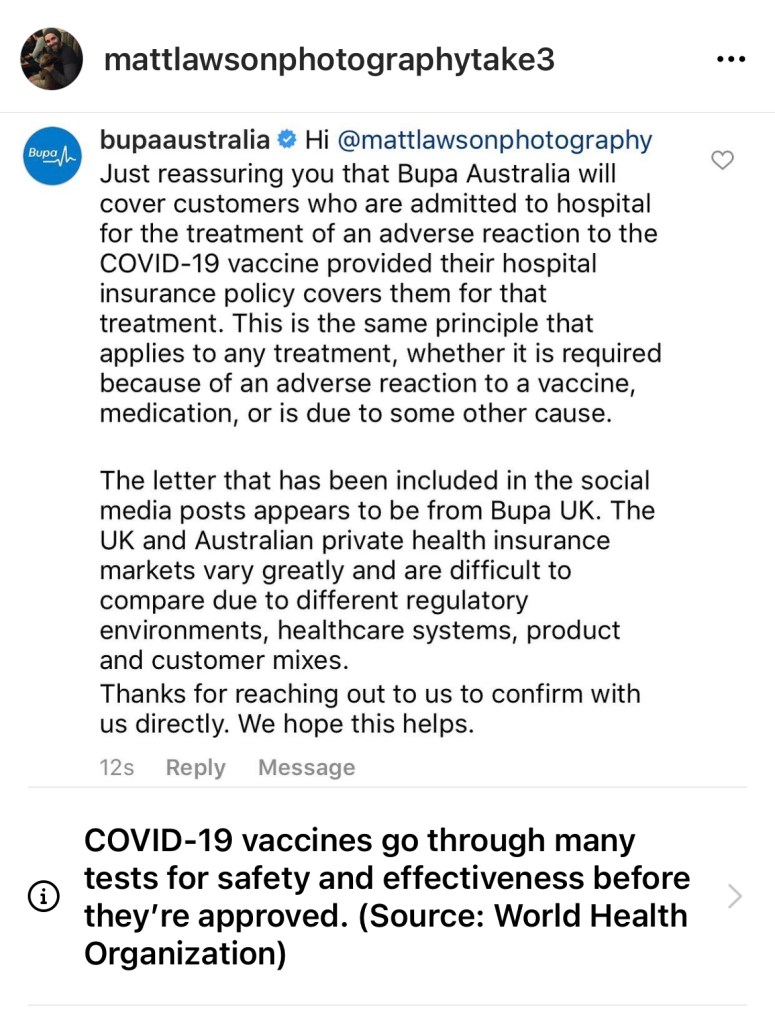

In an interesting twist it was another wannabe COVID conspiracy-freedom-fighter who provided confirmation from Bupa that adverse reactions requiring hospitalisation are covered if their policy covers the treatment provided. It’s a bit of a story so another slide show is needed.

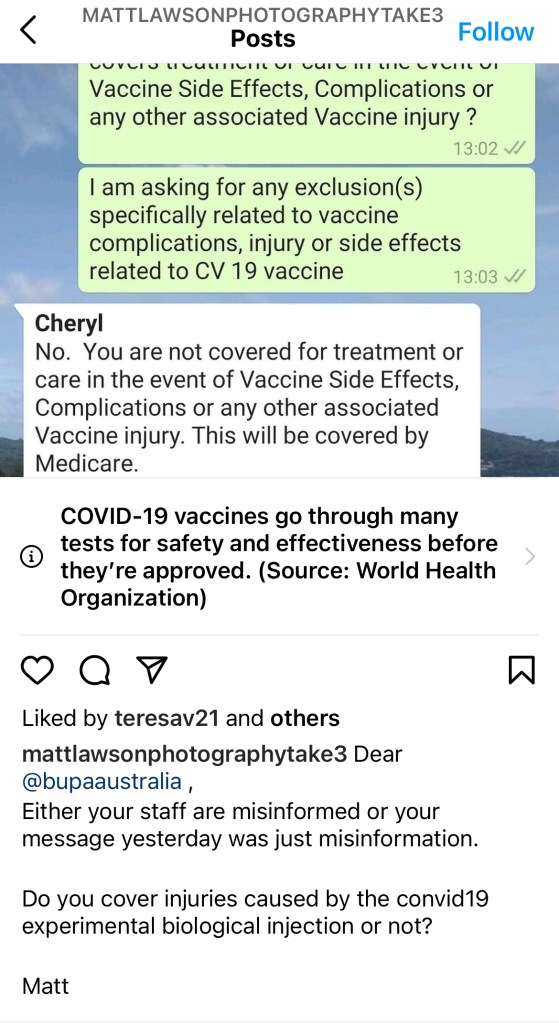

In the first image we see Bupa’s reply to anti-vaccine activist and COVID conspiracy theorist Matt Lawson, on social media. It outlines quite clearly that treatment covered by policy is available for adverse reactions post COVID-19 vaccination. In the next we see Lawson has engaged in a chat with ‘Cheryl’ from Bupa and presented this to Bupa on Instagram to challenge the prior response. The last screenshot was uploaded by Elle Salzone in the thread we’re discussing as another example of an insurance company denying cover to injury or reaction after COVID-19 vaccination.

Yet viewed in context we can see that during the chat Lawson supplied his policy number (image 3). So ‘Cheryl’ was answering in a specific sense, relative to his policy. This is absolutely in line with the claim made by Bupa in image 1 and also with feedback I’ve received from Bupa Australia. Still, image 2 reveals Lawson’s ill-informed, provocative reaction. The theme of acting with aggressive predetermined agendas is ingrained in the new age COVID conspiracy theorists. Matt Lawson reveals his conspiracy theory thinking when he writes;

Do you cover injuries caused by the convid19 experimental biological injection or not?

This comprehensive article reveals Bupa’s support for the COVID-19 vaccine and is in line with the position of global health authorities. There is no suggestion Bupa view the vaccine as experimental. Quite the opposite.

The letter mentioned in Lawson’s Instagram chat with Bupa Australia is circulating in social media within Australia. Within the Elle Salzone’s Facebook thread the image was uploaded twice, in support of the Allianz forgery. One commenter stated, “Another example shared of a void policy”. The second observed, “I think Bupa were one of the first…”. The image is below.

The text is as follows;

23 March 2021

Dear [redacted]

Thank you for speaking to me.

I confirm that side effects arising from the COVID-19 vaccine are not covered under our exclusion for: Complications from excluded or restricted conditions/treatment and experimental treatment exclusion.

If you are injured whilst doing COVID-19 swab yourself, cover would be available towards the injury.

I hope this information is helpful. If there is anything else we can help you with, please call our team on the above helpline number.

Yours sincerely

[signature]

Even if genuine, this letter has no impact on Australians. Peering at the Bupa letterhead we can confirm it is from Bupa Place in Salford Quays, Manchester U.K. Anti-vaccination activists will contend that the first paragraph confirms that side effects and complications from the COVID-19 vaccine are excluded from cover because it is an experimental treatment. The second paragraph conveys that insurance cover is available if one is injured, “whilst doing COVID-19 swab yourself”. In the U.K. home test kits are available.

Australians can also dismiss this as here it is illegal to advertise testing kits for serious infectious diseases. The TGA have a very clear warning to consumers and advertisers on their website. Thus there is no reason for Bupa to even consider such cover in Australia and Bupa members can disregard the letter and its claims.

Still, anti-vaccine claims are global in their reach, as is social media. If we take a cautious and in depth look into the origins of this letter there are different possible conclusions. It is a poorly written fake or a badly written follow up with a customer. Neither confirm the claim of an uninsurable experimental vaccine.

Bupa U.K. explain excluded and restricted cover in this Bupa Membership Guide [Archived]. This document provides a likely source for the information that the author presents with notably poor grammar. The opening paragraph is difficult to grasp. It may be that English is not the author’s first language.

With respect to the terminology used in the letter, on page 35 of the U.K. Bupa Membership Guide we find;

Exclusion 7 Complications from excluded conditions, treatment and experimental treatment

We do not pay any treatment costs, including any increased treatment costs, you incur because of complications caused by a disease, illness, injury or treatment for which cover has been excluded or restricted from your membership. […]

We do not pay any treatment costs you incur because of any complications arising or resulting from experimental treatment that you receive or for any subsequent treatment you may need as a result of you undergoing any experimental treatment.

On page 38 we find under Exclusion 16 Experimental Drugs and Treatment, this paragraph;

Please also see ‘Complications from excluded conditions/treatment and experimental treatment’ […]

There we have it. The text could have been copied and pasted in an extremely poor customer follow up, and that’s it above. Or copied and cobbled together in a dodgy forgery. The antivaccinationist lie of an uninsurable experimental vaccine is quite vocal on social media in the U.K. Yet under the glare of fact it is a demonstrably pointless effort.

In the U.K. COVID-19 vaccine side effects are covered under the Vaccine Damage Payments Scheme, established in 1979. This provides no-fault compensation for Adverse Events Following Immunisation. It is possible that offering cover is not an option for insurance companies. Either way, side effects are not covered by Bupa U.K. So it may well be that treatment of complications is classified as restricted and/or excluded regarding hospital cover.

The most important point here is that the COVID-19 vaccine is not an experimental treatment. Yet this letter is being pushed in Australian anti-vaccine circles to contend insurance companies are of the view it is experimental. Whilst a bogus claim, the overall forgery scam is reinforcing that claim in COVID conspiracy circles.

Bupa Australia are aware of this letter and have taken the chance to assure those who ask (such as the argumentative Matt Lawson) that cover is certainly available. When I raised this specific issue I was informed by Bupa Australia;

Private health care in the UK and Australia can vary greatly. But rest assured that our members will be covered for any hospital admission following an adverse reaction to the COVID vaccine, as long as the service is included in their cover, and any waits have been served.

Ultimately all the anti-vaccine points put forward by Elle Salzone and others on her Facebook page are demonstrably false. A search for insurance cover and COVID-19 vaccine adverse events yields results from around the world, not just Australia. For example cover for AEFI after the COVID-19 vaccine is available in Singapore whilst there’s a WHO compensation fund for people in developing nations suffering side effects. In general, insurance companies are involved in many areas specific to the COVID-19 vaccines, including in China where they are looking to cover adverse reactions.

Sadly some Facebook visitors to Elle Salzone’s page, who take her word on trust, are absolutely convinced of the dark side as this reply to me, packed with five pieces of misinformation, confirms. [Note – this is not from Salzone but a vulnerable visitor].

Sigh. Still all hope is not lost. As the well-known phrase from the X Files reminds us:

The truth is out there.

Last update: 8 April 2021

♠︎ ♠︎ ♠︎ ♠︎